“My understanding of why the FAIR Plan came into being was really to protect the public so that they

would have a place to get insurance when they need it. And that really is the role of government, to

protect the people.” Dan Ryan, Ryan & Walis Realty, testimony at

NYS Assembly Insurance Committee Hearing, 10/22/04

Executive Summary

New Yorkers who cannot find insurance coverage for their properties in the private market must turn to the state’s

property insurer of last resort - the New York Property Insurance Underwriting Association (NYPIUA). NYPIUA was

established in 1968 after riots in cities across the country gave rise to a federal law encouraging states to establish

“Fair Access to Insurance Requirements” (FAIR) Plans. NYPIUA now insures over 57,000 homes

and businesses throughout the state that private carriers have rejected, usually because of the location, age or

condition of the properties.

Since its inception in 1968, NYPIUA has served as the state’s insurance safety net primarily in urban areas

by providing basic fire and extended coverage sufficient to meet the requirements of mortgage lenders. For a host of

reasons, NYPIUA is now also a principal insurer of properties along the state’s coastal areas on Long Island,

where one quarter of its insured properties are located. NYPIUA serves as a true residual market whenever

and wherever property insurance becomes unavailable, much like the “assigned risk plan” operates for

auto insurance and the Medical Malpractice Insurance Plan for medical liability.

NYPIUA has existed pursuant to temporary statutory authority since its inception. Extenders have ranged from several

years at a time to just days. The association’s current authorization expires on June 30, 2005.

Recognizing that NYPIUA has proven its value beyond question and that its temporary nature is no longer justified,

the state Assembly has passed legislation 10 times over the last nine years to permanently authorize NYPIUA, with

the support of consumer groups, insurers, agents, realtors, editorial boards, the state Insurance Department (SID)

and, on two occasions, Governor George Pataki. New York and Alabama are the only states without a permanent

property insurance safety net.

The state Senate has repeatedly refused to agree to anything but short-term extenders of this vital program, sometimes

linking it with other contentious issues. This has resulted in periodic lapses in NYPIUA’s authority, with

damaging human and economic consequences. During these lapses, NYPIUA has had to turn away new applicants

and send out non-renewal notices to existing policyholders, panicking people facing loss of coverage and disrupting

orderly transfers of real estate. NYPIUA’s tenuous history has left policyholders vulnerable in the event of

losses related to catastrophic events, as NYPIUA is unable to establish a line of credit to meet the need for immediate

funds to swiftly settle a large number of claims.

NYPIUA’s importance as New York's insurer of last resort and problems associated with its transient

statutory authorization were the focus of an Assembly Insurance Committee public hearing on October 22, 2004

in Long Beach, New York. The committee sought information as well on the possible impact of the year’s

ruinous hurricane season on insurance availability and cost for property owners in New York’s coastal

communities and NYPIUA’s involvement in these markets. The committee’s announcement and

hearing notice is appended to this report (Attachment A).

NYPIUA policyholders, consumer organizations, insurance agents, real estate brokers and insurance companies

were invited to testify. This report cites the testimony and position papers of witnesses who appeared before the

committee or submitted statements for the record attesting to NYPIUA’s vital role, the human and economic

toll of its periodic lapses, and the overwhelming public consensus for making this essential insurance safety net

permanent.

Supporters of a Permanent NYPIUA

Independent Insurance Agents Association

Professional Insurance Agents Association

Council of Insurance Brokers of Greater New York

New York Insurance Association

American Insurance Association

Property Casualty Insurers Association of America

The Temporary Panel on Homeowners’ Insurance Coverage

(compromised of property/casualty insurance

associations, individual insurers, (compromised of property/casualty insurance

associations, individual insurers,

the Reinsurance Association of America

and individual reinsurers, reinsurance

brokers, and property/casualty insurance agents)

Long Island Board of Realtors

Multiple Listing Service of Long Island

Neighborhood Housing Services of New York City

Community Development Corporation of Long Island

National Fair Housing Alliance

Assn. of Community Organizations for Reform Now (ACORN)

NYC Comptroller William S. Thompson

New York Public Interest Research Group

NYPIUA’s Origin

NYPIUA was formed in 1968 after widespread riots in American cities precipitated enactment of the federal

Urban Property Protection and Reinsurance Act, which made riot reinsurance available to insurers in states that

adopted Fair Access to Insurance Requirements (FAIR) Plans. Since its inception, NYPIUA has served as New

York’s insurer of last resort for homes and businesses that conventional insurance companies refuse to

insure, much like the “assigned risk plan” operates for auto insurance and the Medical Malpractice

Insurance Plan for medical liability.

By providing necessary property insurance for dwellings and businesses when private market coverage cannot

be obtained, NYPIUA assists in attracting investment of private capital, promotes community development and

helps prevent economic deterioration.

NYPIUA is a self-supporting joint underwriting association made up of insurers writing fire insurance policies in

the state. Under NYPIUA’s statute, its insurer members “participate” in the

association’s writings, expenses, profits and losses. NYPIUA’s staff underwrites, rates, issues

and services policies and settles claims on behalf of its insurer members. It operates independently of and

has no relation to the state budget, and has never been linked with state budget negotiations.

Insurance NYPIUA Provides

NYPIUA provides basic property insurance for residential and commercial properties sufficient to meet the

requirements of mortgage lenders. Included in NYPIUA’s package are fire and extended coverage

such as windstorm, vandalism and malicious mischief, and sprinkler leakage; and time element coverage

including loss of rent and business interruption insurance. The association does not provide liability coverage.

Rates are generally 20% to 40% higher (according to class of business, as prescribed in statute) than those

charged in the voluntary market.

NYPIUA also plays a major role in New York’s coastal areas by insuring the windstorm portion of

policies which are “wrapped” with the remaining coverages provided by private market insurers.

These policies are written under the NYPIUA-administered Coastal Market Assistance Program (CMAP).

Nearly 4500 C-MAP policies have been issued for one- to four-family dwellings, including condominiums

and cooperative apartments in areas of Long Island, Brooklyn, Queens, the Bronx, Staten Island and Westchester

that are close to the Atlantic Ocean or Long Island Sound.

Who NYPIUA Serves

Because there can be numerous features of a property, other than proximity to the ocean, that insurers

consider too risky to insure, NYPIUA’s 57,000 policies cover properties located throughout the state.

Anyone who owns or seeks to buy a building that is older, in disrepair or frequently vacant, or located in or

near a neighborhood insurers believe is blighted, a rural area where fire department service is considered

less than optimal or in a community on or near the state’s coastline - is likely to have to turn to

NYPIUA for property insurance at some point. NYPIUA also serves people who cannot find insurance

because of their “poor” credit history or a record of multiple claims.

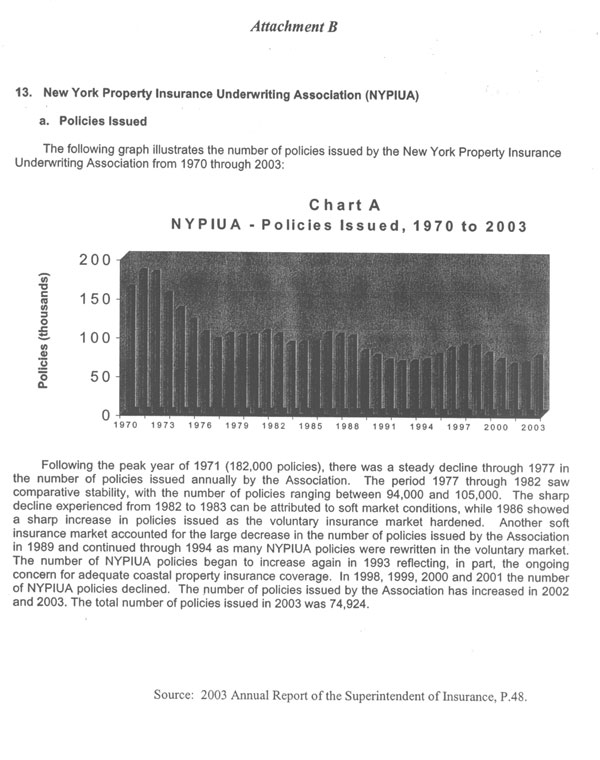

Established initially to insure properties in inner-city communities, NYPIUA has come to act as a true residual

market whenever and wherever property insurance is unobtainable in the private market. While the number

of those who have had to resort to NYPIUA has declined since association policies peaked at 182,000 in

1971, NYPIUA has seen spikes of policy growth when, for varying reasons, insurers become more selective

about the kind of properties they will cover (Attachment B).

NYPIUA quickly became an essential substitute for private market insurance during the mid-1990s in

New York’s coastal areas, particularly on Long Island, an area insurers had previously considered

profitable. Because of huge losses caused by Hurricane Andrew in 1992, insurance companies reevaluated

their policy concentrations along the entire eastern seaboard. In an effort to reduce their exposure to further

storm losses, insurers moved aggressively to drop existing policyholders, stop issuing new policies, raise

prices, add hefty deductibles and phase out coverage that guaranteed the full replacement of insured property.

As a result of this market retrenchment, NYPIUA experienced a surge in new policies along New York’s

coastal areas from 1993 to 1998. This was felt most heavily in Long Island, where, for many of the 14,000-plus

current NYPIUA policyholders in Nassau and Suffolk counties, NYPIUA remains the only insurer in the marketplace,

a point highlighted at the hearing by local business owners:

“I would appreciate if Assemblyman Grannis and Assemblyman Weisenberg would no longer refer to New

York Property as the insurance company of last resort. This is the insurance company of first resort. . . I use them

as a primary company.” Denis Miller, President, Denis A. Miller Insurance

(an independent insurance agency in Long Beach), Assembly hearing

From 2001 to 2003, NYPIUA again proved vital when the confluence of the stock market collapse and staggering

losses from the September 11 terrorist attacks led the property and casualty insurance industry to tighten its

underwriting to make up for investment losses and limit the potential for claims from further attacks. During this

period, NYPIUA saw a 142% increase in new commercial policies.

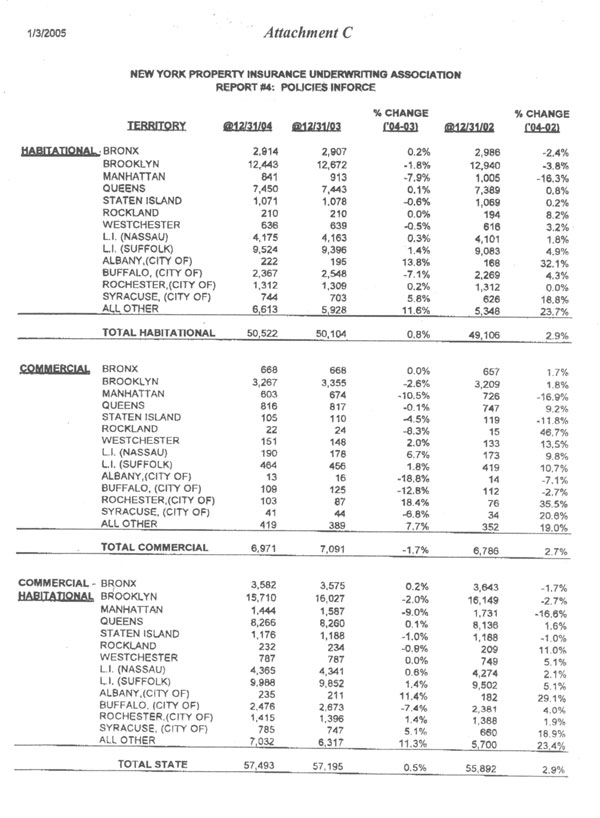

Today, NYPIUA provides vital insurance for more than 50,000 residential properties and nearly 7,000 commercial properties

throughout the state. Detailed on Attachment C and summarized here is the distribution of NYPIUA policies in force:

|

Policies

|

% of

NYPIUA Book

|

|

|

New York City:

|

30,000

|

52%

|

|

Long Island:

|

>14,000

|

25%

|

|

Rockland/Westchester:

|

1,000

|

2%

|

|

Alb, Buff, Roch, Syr:

|

5,000

|

9%

|

|

Rest of State:

|

7,000

|

12%

|

A significant number of these policies are secured for consumers on a short-term basis. NYPIUA’s role as

an important facilitator of homeownership and real estate transactions was underscored at the hearing:

“NYPIUA has an important place in homeownership, providing a temporary haven for those risks that the

standard market cannot carry. NYPIUA gives homeowners the ability to borrow the money needed to bring their

property up to reasonable condition and/or the time to improve their loss history. It relieves the onerous burden of

a forced place policy.” Elizabeth Malone, Insurance Services Program Manager,

Neighborhood Housing Services (NHS) of New York City, Assembly Hearing

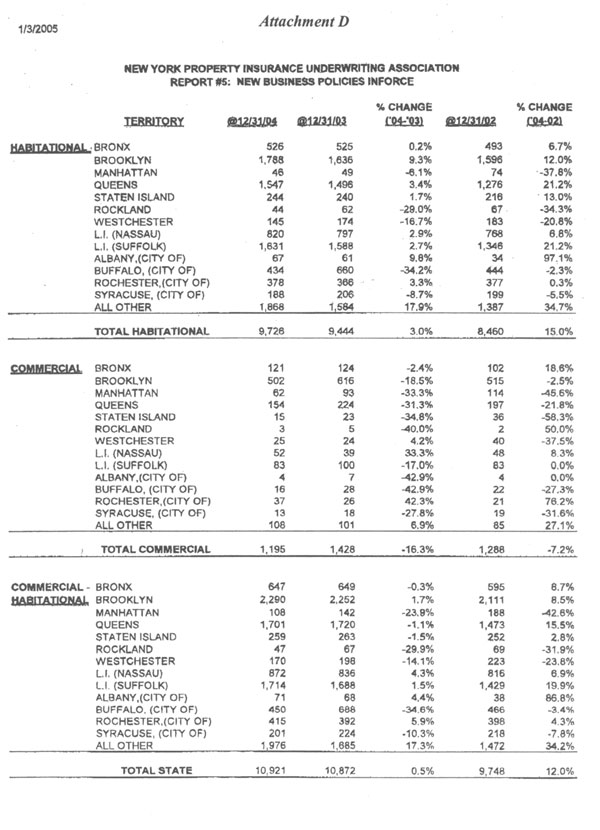

Highlighting the importance of short-term access to NYPIUA coverage are policy numbers from

2003 (Attachment D). In 2003, NYPIUA issued 74,924 policies, with 57,195 of these

remaining in force at year’s end. The difference reflects the thousands of New York residents who

were able to move from NYPIUA into private market insurance during the year. NYPIUA is the indispensable link

in this transition, promoting loss control measures through its matching grant program for electrical repairs and

other means to help policyholders improve the safety of their properties.

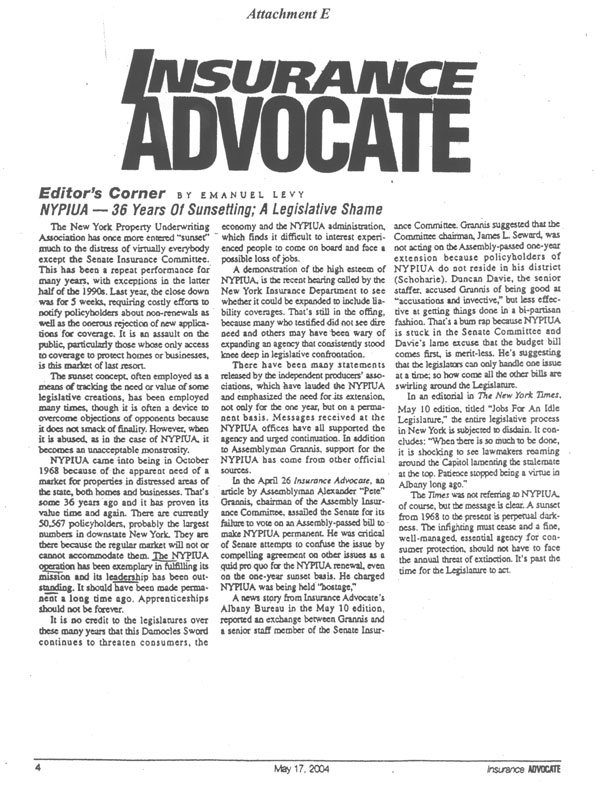

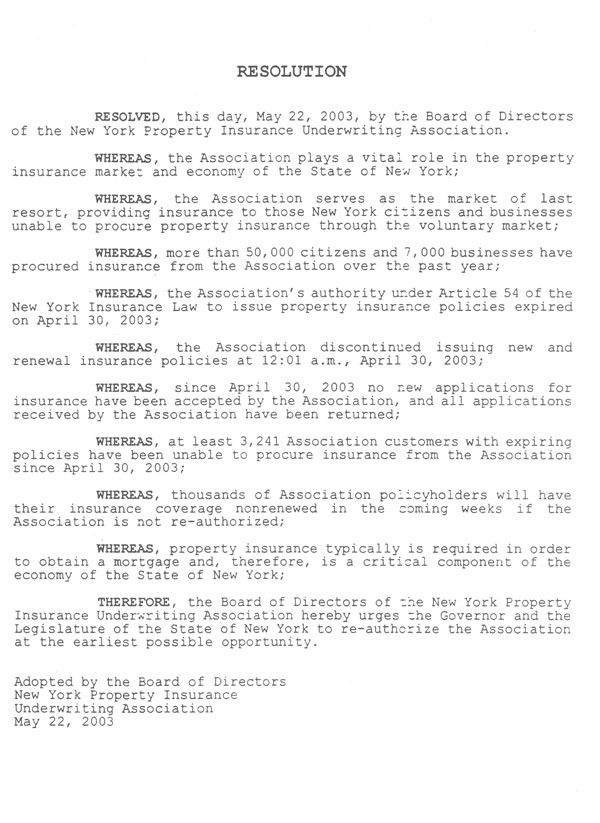

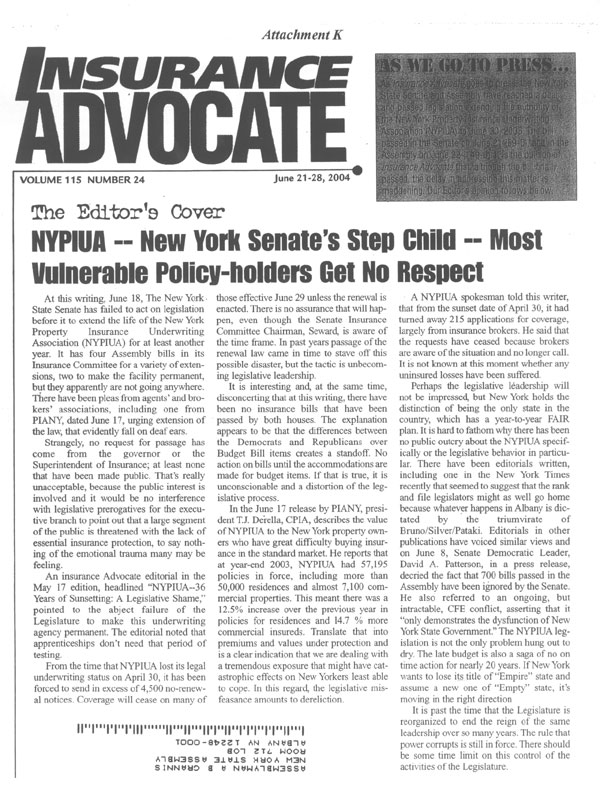

“NYPIUA – 36 Years of Sunsetting; A Legislative Shame”

“The sunset concept, often employed as a means of tracking the need or value of some

legislative creations, has been employed many times, though it is often a device to overcome objections

of opponents because it does not smack of finality. However, when it is abused, as in the case of NYPIUA,

it becomes an unacceptable monstrosity. . ..[NYPIUA] has proven its value time and again. . .Apprenticeships

should not be forever.” Insurance Advocate, editorial,

“NYPIUA – 36 Years of Sunsetting; A Legislative Shame,” 5/17/04,

(Attachment E)

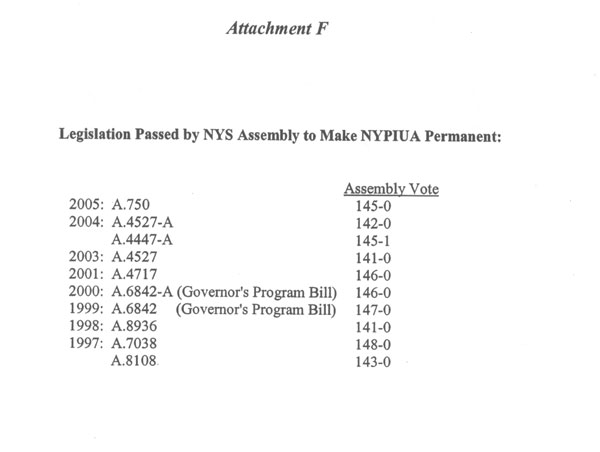

The Assembly has passed legislation on 10 separate occasions since 1997 to make NYPIUA permanent

(Attachment F), a goal Newsday says “makes sense”

(Newsday editorial, “Late again. . .and again,” 4/20/04). By refusing to do anything but

short-term extenders, and at times attempting to link NYPIUA extenders with controversial

issues,* Senate leaders have permitted NYPIUA’s authorization

to lapse periodically before belatedly signing off on short extensions. As the result of these tactics, reflecting

a glaring indifference to the human and programmatic fallout, Senate leaders have precipitated two extended

and harmful NYPIUA shutdowns: 56 days in 2003, and 53 days in 2004.

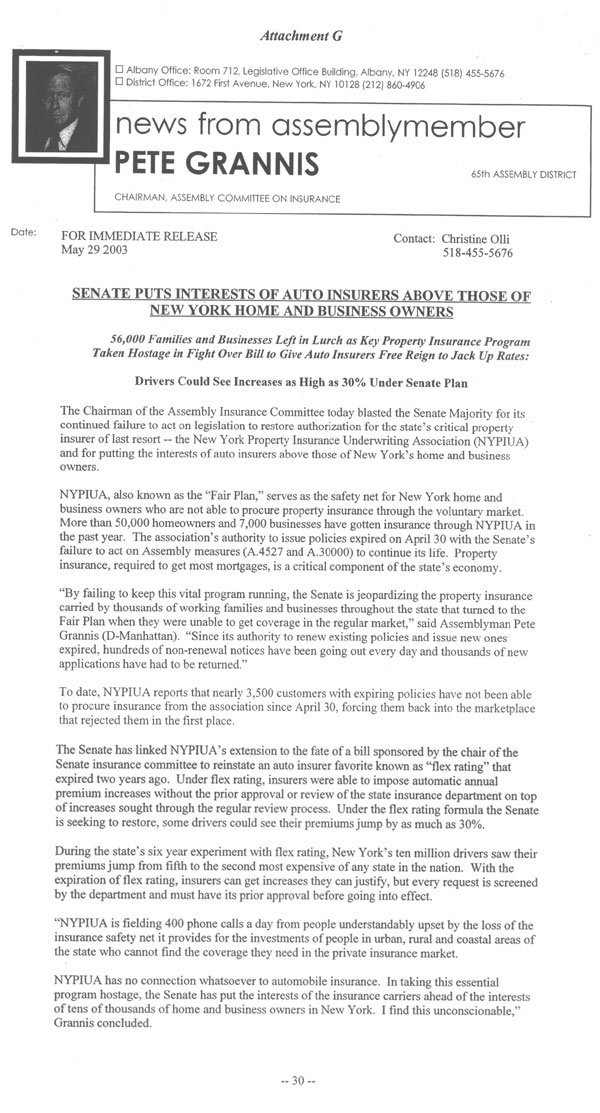

*In a 2003 effort to deliver

guaranteed rate hikes for auto insurers, the Senate held NYPIUA hostage by linking its extension with an

insurer favorite known as “flex rating,” which lets companies raise rates automatically every

year without prior approval of the Insurance Department (Attachment G).

In the midst of the nearly eight week gap in NYPIUA’s authority in 2004, the Insurance Advocate

targeted the Senate’s role in obstructing Assembly legislation to make the program permanent:

“The New York Property Insurance Underwriting Association has once more entered “sunset”

much to the distress of virtually everybody except the Senate Insurance Committee.”

Insurance Advocate, editorial, 5/17/04

The Senate has set the limited periods of each of NYPIUA’s extenders since the easing of the coastal

insurance crisis following reforms advanced by the Assembly and enacted into law in 1996. At no time has any

Senator or staff member identified any problem or expressed any need or desire to review or tinker with this program.

The excuses offered by Senate leaders for permitting only short-term NYPIUA extenders ring hollow:

“This is a two month extender. And this short-term extender will give us a better opportunity to

further evaluate the proper term for the next extension of NYPIUA.” Senator James A. Seward,

Chairman of the Senate Insurance Committee, floor debate on his bill to extend NYPIUA for two months (S.7181), 4/27/04

“With the current law’s sunset date and its proximity to the State Budget process, it has caused

an unproductive entanglement that S.7181 would resolve. Prospectively, extensions employing this June date

would substantially diminish the likelihood of similar situations in the future.”

Letter from Long Island Senators to their Assembly counterparts, 5/27/04

“The program’s been extended while we deal with other issues. . .We have a budget we’ve

got to resolve and that’s certainly front and center. . .Once we get some of these issues out of the way

we’ll be able to focus on the future of NYPIUA.”

Senate spokesperson, Insurance Advocate, 5/10/04

“State Senator Dean Skelos (R-Rockville Center), the Senate Deputy Majority Leader, said the

extension would provide time to tackle much-needed changes to other types of insurance. He also said that he

favored reauthorization in two-year stints so that “you can see if there are ways to improve the program.”

Newsday, “Property Owners in a Bind,” 5/14/04

In refusing to make the program permanent, Long Island Senators rejected the call of their Assembly colleagues

(Attachment H), turning their backs on the 14,000-plus Long Island property owners and the

region’s agents and realtors who depend on NYPIUA’s insurance. This point was highlighted

repeatedly during the committee’s hearing:

“This year, as always, the Assembly has forwarded a bill which would make coastal insurance available

on a permanent basis. . .[T]he 23,000 members of LIBOR have asked on numerous occasions the [Island’s]

Senate delegation to pass a companion bill so that we don’t have to face this deadline again.”

Randy Kaplan, Director of Government Affairs, Long Island Board of Realtors (LIBOR),

Assembly hearing

The Toll of NYPIUA’s Lapses

The most recent lapses of NYPIUA's authority stretched for weeks. In each instance, the association had to turn

away hundreds of applicants seeking coverage every business day, and send out thousands of non-renewal

notices to existing policyholders, throwing families to the mercy of the very marketplace that rejected them in the

first place. During the shutdowns in 2003 and 2004, NYPIUA sent out over 12,000 non-renewal notices.

Shutdowns needlessly burden agents with the extra work of seeking replacement coverage for their clients,

and force property owners to confront the prospect of exorbitant costs of force-placed or excess lines coverage,

or going without any coverage at all.

In addition to their toll on property owners, these breaks in statutory authority cause anxiety for NYPIUA staff

over their employment status, and hamper the association’s ability to recruit experienced personnel.

They also waste NYPIUA’s resources in reprogramming systems, fielding calls, and issuing and

mailing nonrenewal notices and replacement policies.

Aside from interrupting the writing of basic property insurance, NYPIUA’s lapses trigger the suspension

of the special program that serves New York’s vulnerable coastal communities – the Coastal

Market Assistance Program – including the issuance of “wraparound” policies.

Finally, these shutdowns jeopardize NYPIUA’s standby powers to write additional lines of insurance at

the direction of the state Insurance Superintendent should meaningful coverage become unavailable in the

private market. In response to a crisis in the cost and availability of liability insurance, NYPIUA was given standby

powers in 1986 to write certain commercial risk, public entity and professional liability insurance. Similar standby

authority to issue homeowners’ insurance was enacted in 1996. Though these special powers have

never been invoked, they would be unavailable should they be needed during any shutdown.

Witness testimony speaks to the scope of the human impact of NYPIUA’s lapses:

“NHS of New York City issued a position paper this past June supporting the bill for making

NYPIUA permanent and we stand by that position. At NHS, we see the worried senior citizens who do not know

what to do when their non-renewal notices arrive. We see the repairs delayed while the rehab loans are held

up for lack of coverage. We see months’ worth of forced-placed insurance charged to struggling families

as their access to the plan is denied. And we see how this burden falls on the very neighborhoods the plan is

designed to aid and undermines the progress these communities have worked so hard to achieve. . .The failure of

the State Legislature to make [NYPIUA’s] authority permanent has an adverse and disproportionate

effect on the communities that NHS serves.” Elizabeth Malone, Insurance Services

Program Manager, NHS of New York City

“Each day that NYPIUA is unable to carry out its responsibilities, over 100 Long Islanders will go

without insurance on their properties and/or be unable to buy or sell their homes. The lack of available insurance

also results in many last-minute costs and inconveniences, including the rescheduling of moving vans and

additional unexpected time off from work. . .The bottom line is that’s dollars that are coming out of

people’s pay and that hurts. . ..As the lobbyist for the realtors, I can’t tell you how many members

have called me throughout the course of the years in panic. What do we do? How many homeowners have

called us because they were referred to by realtors asking what do we do? We don’t know what to do.

We’re stuck. Help us. Please help. There’s nothing we can do.”

Randy Kaplan, Director of Government Affairs, LIBOR

“. . .the sunset law every year – I can put a real face on the problem. . ..There are buyers that have got to

move. They can’t move. They can’t get in. Their housing is affected. They have moving vans

ready to go. Their rates that they have on their mortgages start expiring. Sellers that have to buy other houses

are affected. The domino effect is incredible. It really does create a major problem financially for the people,

and. . .this is not supposed to happen. In addition, what it does is buyers that even come down here and

even hear about it, it gives them pause. . .More than 75% of the deals that I do. . .they need to go through

NYPIUA. . .and they’re going to [hesitate] where we might have five, six weeks where they don’t have

insurance. It’s a catastrophe. . ..I think in general everybody would understand that the housing market

is very important to the economy and what it does for the economy, and any hiccup in that can only be a negative

effect. . .One of the main reasons I’m down here was to go on record to state that the broker community,

the Long Beach Chamber of Commerce, the MLS, would like to see this be a permanent thing. It seems

ludicrous. You asked a question a few minutes ago and there was no response if there was any reason why

it isn’t happening other than it’s a political football. That hurts. The public doesn’t want

to hear that when the largest asset that they have, which is their home, is being tossed around. One major

storm, whatever came sweeping through here during that period, would be devastating. I just wanted to go

on record how strongly we support that [NYPIUA] be made permanent.”

Dan Ryan, Ryan & Walis Realty

Disaster Preparedness Impossible Without a Permanent NYPIUA

NYPIUA has other duties and authorities, which, as a practical matter, it cannot carry out because of its temporary

and tenuous legal position. Notably, NYPIUA cannot properly prepare to settle claims in a timely manner in the

event of a large-scale catastrophic storm. The Temporary Panel on Homeowners’ Insurance Coverage,

established at the direction of the Legislature in 1996 to examine and assess the problems affecting the

availability and affordability of homeowners insurance in the state, highlighted this in its first report to the

Governor and Legislature:

“NYPIUA has the power to assess insurance companies when it needs funds, but in the aftermath of

a major catastrophe it would need cash faster than an assessment could deliver. The NYPIUA Board has

sought a line of credit to be in a position to meet a sudden large cash drain. However, financial institutions

are reluctant to grant such a line of credit because of the short term for which NYPIUA is presently authorized

by statute.” Report of the Temporary Panel on Homeowners’

Insurance Coverage, 10/01/96

Similarly, the Professional Insurance Agents Association’s 2004 position paper highlights how

NYPIUA’s time-limited existence interferes with its ability to enter into long-term contracts needed to

execute its statutory authority to secure reinsurance:

“Another reason to give NYPIUA permanent status is that it cannot reach its full potential living

from year to year. When catastrophic property reinsurance became scarce following Hurricane Andrew, it

was not feasible to consider NYPIUA as a mechanism for obtaining reinsurance on behalf of its members,

even though it is legally empowered to do so.”

The Pataki Administration – Missing in Action

Despite voicing support for a permanent program, including advancing legislation in 1999/2000, the state

Insurance Department and Governor Pataki appeared stunningly apathetic during the latest multi-week

lapses of NYPIUA’s authority. Letters from Chairman Grannis to Governor Pataki calling for leadership

on this issue went unanswered (Attachment I). Resolutions from NYPIUA’s Board

of Directions were ignored (Attachment J). The Insurance Advocate focused on the

administration’s abdication of responsibility in its second editorial last year calling for a permanent law:

NYPIUA – New York Senate’s Step Child – Most Vulnerable Policyholders Get No Respect:

“Strangely, no request for passage has come from the Governor or the Superintendent of Insurance; at least

none that have been made public. That’s really unacceptable, because the public interest is involved

and it would be no interference with legislative prerogatives for the executive branch to point out that a large

segment of the public is threatened with the lack of essential insurance protection, to say nothing of the emotional

trauma many may be feeling.” 06/21/04, (Attachment K)

At the committee’s hearing, the following exchange between Chairman Grannis and Insurance Department

Deputy Superintendent Joe DeMauro substantiates the Advocate’s description of the administration’s

abandonment of its role in protecting the interests of the thousands of working New York residents who depend

on NYPIUA for their property insurance:

Grannis: In the past, the Administration has submitted bills to make [NYPIUA] permanent. We’re

the only state other than Alabama that does not have a permanent FAIR Plan. It’s a disgraceful situation.

Do you intend to submit a departmental or Governor’s Program Bill in the upcoming legislative session to

make it permanent?

DeMauro: Given the difference of opinion on the permanency of NYPIUA in the Legislature, we don’t

see how a Governor’s Program Bill or departmental would make any difference until you guys resolve the

differences between the Senate and the Assembly.

Grannis: The governor is the leader of the state; you’re in the agency in charge of making

sure that the market functions properly. . .There are probably 100 different bills sent up by the administration

on which there are vast differences. The administration puts in bills all the time on things that it believes are the

correct things to do.

DeMauro: We certainly are concerned about the gaps and we don’t want to see any lapses

as the Department. However, how you get there is really a legislative policy decision.

Grannis: Absent any leadership from the administration.

DeMauro: As I said, we are concerned about lapses and we don’t want to see NYPIUA lapse.

Conclusion

NYPIUA’s current statutory authorization expires June 30, 2005. With only two exceptions, New York

and Alabama, every state has made its property insurance safety net permanent, recognizing that there will

always be properties or consumers that insurance companies will not insure in the conventional marketplace.

Property insurance is an absolute necessity for people pursuing the dream of buying a home or running a

business and protecting what is often the biggest investment of their lives. Property insurance is essential to

allow homes and small businesses that are destroyed or damaged to be rebuilt, to keep neighborhoods

from sliding into decline, and to revitalize neighborhoods by encouraging the improvement of buildings with

substandard conditions. NYPIUA has served its purpose in addressing these goals unfailingly during its nearly

four decades of operation.

New Yorkers need to know that insurance will be available to protect their homes and businesses.

If the coverage they need is denied them in the conventional market, they should not be victimized a second time

when the standby coverage they secure through NYPIUA is pulled from under their feet by the needless lapse of

the association’s authority. It is time to end the misguided use of this vital program by the state Senate

as a political football in its dealings with the Assembly. It is time to make NYPIUA permanent. There is overwhelming

support throughout New York for doing so this year.

|